Agriculture

HOW LOW CAN CORN GO?

The USDA report suggested farmers last spring paid attention to lower fertilizer costs and higher December corn values by planting more corn. Historically, when crops are planted quickly more corn acres are added at the expense of beans.

Harvested vs Planted Acres

Digging deeper into Friday’s report, the USDA’s harvested acres as a percent of planted seems to mirror the average from 2013 through 2017 instead of the last five years. If the average of the last 10 years was used instead, there would be a 500,000-acre reduction for total production. If the average from the last five years was used, it would reduce harvested acres by 1 million. This could mean a potential carryout reduction of 90-180 million bushels or 5-10% decrease sometime in the future.

Sorghum planted acres were up nearly 1 million from spring estimates, which will directly compete with corn in feed rations across the southern states unless the Chinese buy it for feed or alcoholic beverages.

Feed Category

The USDA also reported old crop corn stocks being tighter than previously estimated. Therefore, it seems likely the old crop feed category will be increased by around 150 million bushels. If this is where the changes are made then it will more closely align with the actual animals on feed, this past year. This old crop reduction may carry through to new crop carryout and help keep numbers from getting completely out of hand.

However, new crop could face some feed demand issues. To hit the current feed estimates, cattle numbers would need to increase, with hog and poultry numbers not dropping. A corn price decrease could spur that kind of growth, but if yields drop and prices rally, it would be difficult for demand to increase.

Exports

This past year export pace was hit when Brazil grew a big crop and US prices were too high. US prices are still higher than our competitors, which will not help increase demand any time soon. This category could be the hardest to hit and ultimately be the reason that corn struggles to rally long term.

July Weather

This continues to be the big unknown. Generally, forecasts are indicating widespread favorable weather in the month of July, but they need to be verified. Forecasts this past month have not always held up.

However, social media can sometimes exaggerate local weather events, making it difficult to understand actual damages. For example, there was a recent derecho in the central Midwest where pictures of wind damage were shown online. While those hit hardest can face some big challenges, there is a high probability that the rain from this storm had more widespread benefit than the actual loss of any crop.

Projecting Carryout and Prices

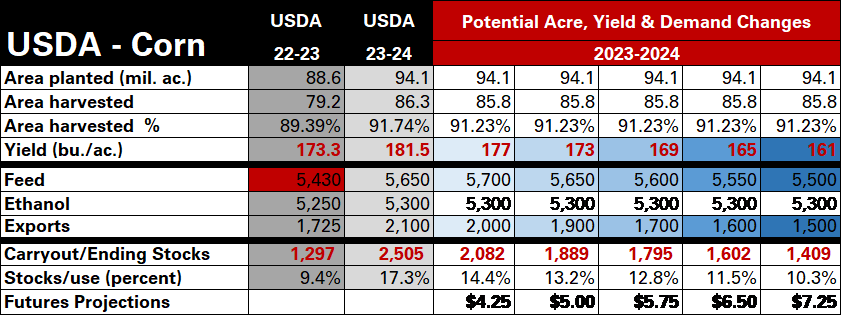

The chart below summarizes the USDA categories that I think will have the most impact on prices moving forward. Also included are my futures price projections based upon different national yield averages.

It seems the market is trading around a 175 per bushel yield today, so any further reduction of the national yield would likely spark a rally. Unfortunately, rallies do ration demand so as the supply is cut so too will eventually the demand be lowered on a rally. A 2-billion-bushel carryout is too much. Anytime in the last 10 years carryout exceeded 2 billion at the end of season, futures fell below $4.

Comparing December Futures – 2012 & 2013 vs 2023

Whitetail Season is Here - Save up to 33% at Cabela's!

Whitetail Season is Here - Save up to 33% at Cabela's!